The Inflation Mirage Distorting Multifamily Performance

I am seeing a clear trend in the slowdown of workforce housing transactions, and it goes beyond higher capital costs. Many sponsors highlighted strong rent growth over the past five years but did not fully account for how inflation pushed operating expenses higher at the same time. Insurance played a major role, but I continue to see budgets that priced controllable operating expenses far below what their assets realistically require.

This is why my data‑driven work matters. It protects LP from investing in deals that are doomed from the start, and it protects GP clients who may be too naïve to know the difference.

I also help GP’s who are already deep into the ongoing operations of an investment property and need an asset manager who can identify past underwriting misses, not point fingers or place blame, and get started immediately in guiding the property (and team) back toward its goals.

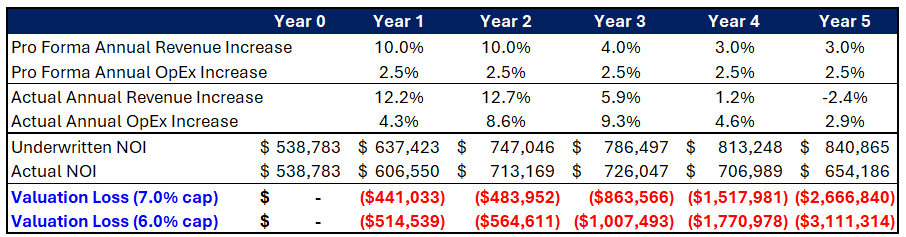

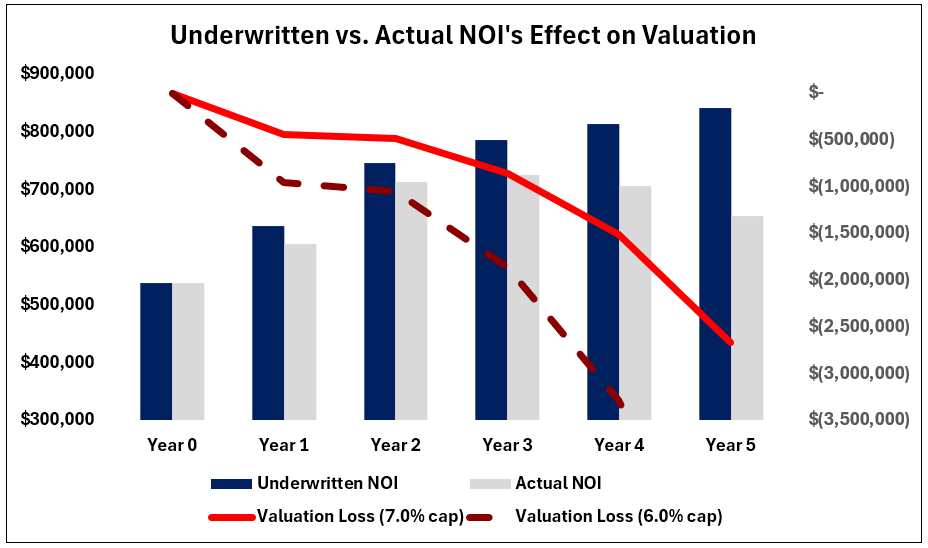

The chart below represents an anonymized multifamily deal. On paper, the revenue story looked strong - rents outperformed the pro forma by an average of 2.3% per year in the first three years. But expenses told a different story, growing 4.9% faster than underwritten. That gap had a far bigger effect on performance, squeezing NOI and pushing valuations below exit expectations.

Some sponsors who expected to exit deals by now are still holding assets, navigating a slow market, tighter 1031 timelines, and more selective, smarter, investors. Groups that entered at 5.0% cap rates with a planned 5.5% exit (like this anonymized example above) find they now require a 4.28% stabilized, terminal cap rate to achieve original pricing assumptions - a level that is not attainable in the current environment and is highly unlikely to return.

I remain optimistic that value creation is still possible in these assets, and that with the right tools, attitude, and collaboration - we can improve struggling investments and deliver turnaround strategies for partnerships. With honest expense assumptions, disciplined operations, and a clear understanding of the numbers, there is still real opportunity for both LPs and GPs to create long‑term value.